Were the Mag 7 more like the Lag 7 in Q2 2026?

Now Playing

Were the Mag 7 more like the Lag 7 in Q2 2026?

Transcript

231 segments

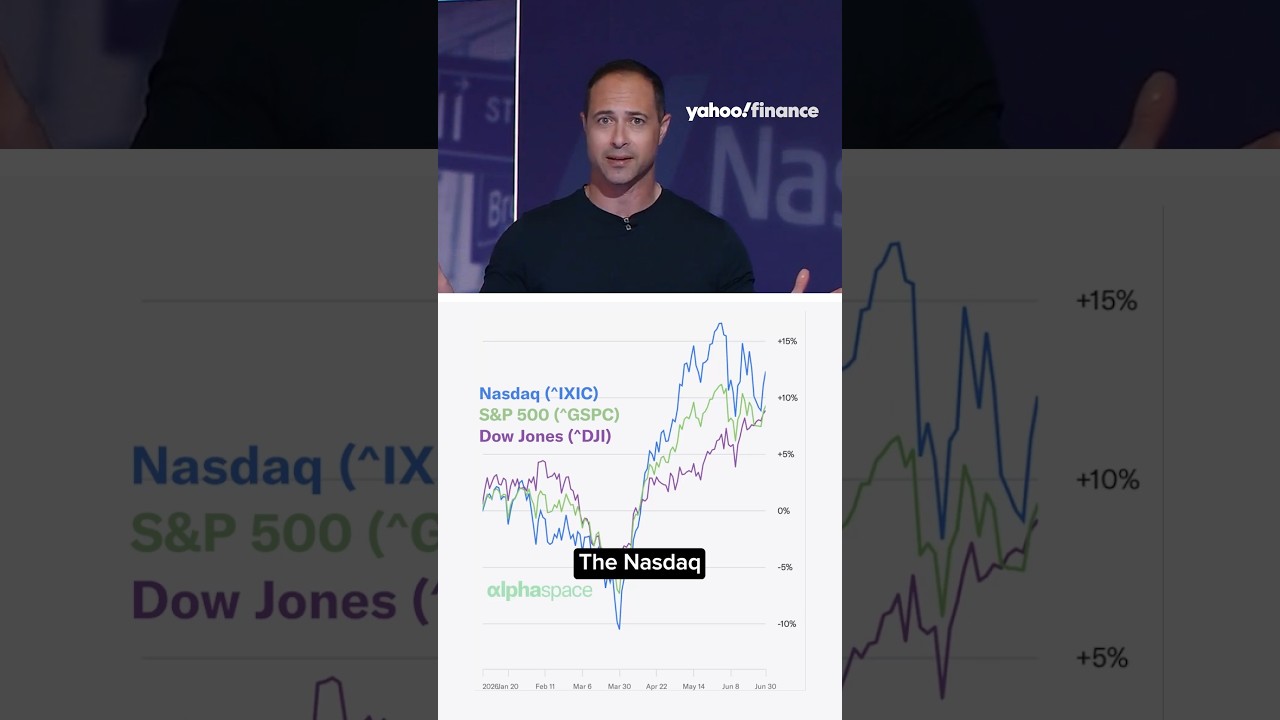

Lee, uh, we are exiting the second

quarter with some big gains. S&P 500 and

NASDAQ. Can these gains continue?

>> I think they can, but I think that the

narrative is going to change a little

bit. This is less about the earnings

bubble in Micron. God bless those

traders. I hope it lasts for another

three, four, five quarters. But I think

investors are starting to talk about and

why we have the Mag 7 becoming the lag 7

is what are people getting for buying

all those pickaxe and shovels. Microsoft

is down, you know, over 20% for the

year, about 35% from its high water mark

because it is the most important company

in the world because if Microsoft can't

turn C-Pilot and Azour AI into

accelerating profits, we have a lot

bigger problems going into 2027. They're

the poster child of if we're going to

get return on, you know, hundreds of

billions of dollars from the

hyperscalers. So, I love that the market

is broadening out, but eventually this

AI trade is going to have to start

hitting hospitals, manufacturing banks,

and small businesses. I think it can,

but the proof is in the pudding. We

haven't seen that yet. Dan, you are our

resident uh tech whisperer here. What

stood out to you in this quarter? I

look, there were a lot of positives, a

lot of interesting new developments,

companies coming out with an amazing

array of whisbang new products, but for

me, one of my takeaways is memory

prices. I mean, these things just keep

going through the roof.

Yeah, obviously that's kind of the the

big to-do right now. Uh and it's a

direct result of this AI buildout. I

mean, you can't have one without the

other. Uh you know, we're seeing

consumers now taking some hits. Uh I'm

doing a piece now on what this means for

it spending uh going into the uh the

couple of quarters ahead. Uh you know,

whether or not we saw companies purchase

before this was all supposed to land. Uh

we've seen companies uh like laptop

makers, smartphone makers uh they're

buying early uh bringing shipments over

uh to get ahead of this so that they

wouldn't have to raise price or at least

take that that price bump and then that

potential uh sales destruction. And so

that's that's probably the biggest

thing. The the other obviously from the

quarter is you know I mean it doesn't

impact what's happening necessarily uh

but the confidential filings for openai

and anthropic uh you know now according

to the times openai may delay its uh

public debut till next year uh but we're

still waiting on anthropic they could

still go public this year and I think

that that's something uh that really is

is worth watching and then obviously you

know the the big kind of now overarching

story is what happens with Q2 is you

know you kind of uh you guys were kind

alluding to is, you know, okay, so we

have all these these big sales going on

with with the chips. Uh what does this

mean for for the actual software? Do are

people getting the productivity they

want? Are we seeing these companies that

sell the software actually perform well?

Uh what's that growth look like? Because

look, they they've had growth there.

We've seen Azure grow. We've seen Google

Cloud Platform grow, uh AWS, but what

what is the direct impact of AI on that?

And then how are other companies using

it? So, not just it's being purchased,

but is it being used and then that's

helping companies become more productive

or are they purchasing it and saying

this isn't really for us right now.

>> Peter, another quarter where AI

investments have been uh really going

with reckless abandon. And we come out

of this quarter with a lot of uh these

big cap hyperscaler companies investing

more in capex and then when they plan

coming into the year, what has been the

influence of these investments on the US

economy?

Well, it's been, you know, very

stimulative both because the capital

spending itself has supported the

economy, but more importantly from the

wealth effect, US households currently

hold around 75 trillion in equity

wealth. Just as a comparison, at the

peak of the dotcom bubble in 2000, they

held 12 trillion in equity wealth. So,

we've gone from 12 trillion to 75

trillion as a share of GDP. That's about

100% higher today than it was back then.

So, households, at least those who hold

that stock, are feeling emboldened to

spend more. Uh the savings rate has

fallen to very low levels, and that's

held up the economy even in the face of

very, very stagnant real income growth.

Year-over-year, real income growth is

actually flat. Consumption is up about

2% largely because of that wealth

effect. Peter, we've seen, and I thank

you for doing this because you teed me

up for it, and you didn't certainly

didn't plan on doing so. Uh, the

K-shaped economy, uh, continues to be a

focus for a lot of investors where, you

know, the higher income is is getting

wealthier, lower income is just

essentially the other side of the K.

It's not looking good. Does that

K-shaped economy continue into the back

half of the year? And what should, you

know, what would that mean to the

economy and to the markets if it does?

Yeah, I mean keep in mind that that the

wealthiest 1% of US households hold 50%

of the stock. So there are large

segments of the population that aren't

really benefiting that much from AI. In

fact, you can argue that they're being

hurt because they're paying more for

memory when they buy a phone. They're

paying more uh for electricity uh

because of the data usage that uh data

centers require. So that's that's a

problem. And if you look at consumer

delinquency rates, they're actually not

that far off from where they were at the

peak in the Great Recession. That's true

for credit card loans. It's true for

auto loans. So large parts of the

population are struggling. If the AI

trade were to go in reverse, I'm not

saying that's going to happen

imminently, but if it were to happen,

then there's a real risk that this

K-shaped economy will end up with an

like looking like an L-shaped economy

where both sides of the K are looking

very very weak.

>> Lee, you know what amazes me? It's and

maybe I shouldn't be amazed. We've been

doing this for a while. Uh how the the

market uh is up double digits in the

second quarter, at least if you look at

the NASDAQ, S&P 500, and it's ignoring

the other side of the K. those lower

income shoppers that throughout the

second quarter dealt with higher gas,

higher food prices, you name it. And

it's just remained so fixated on the the

the comingings and goings of that high

income consumer. How long could this

last market pays attention to the other

half of the population?

>> Well, I think it's you know, you come

down to is the market structure there?

How what size of market cap is Dollar

General and Walmart and McDonald's of

the the general economy? I would say

that when you start looking at it, it

might appear structurally that the lower

spenders have less exposure to publicly

traded company earnings uh say in the

S&P 500, but eventually this is going to

start pressing on us. I think the more

important thing versus the lower in

consumer which I think is I think the

market is more insulated from that. But

you're going to need those people to

adopt AI. you know, you're going to need

those people to keep spending on

subscriptions of things like Netflix and

whatever the 20 bucks that you know that

what new AI service they they need to

get everybody to spending on to make

this stuff profitable. But I think the

big issue is going to be the rate hikes

at the end of this year. And even if we

don't get that, uh, eventually people

are going to realize that the Fed is not

going to be cutting aggressively. I

think we all know that. But it is going

to start weighing. And when you look at

companies that were thinking about

getting interest rate relief that's

going to accelerate EPS going into the

end of the year, those dreams are

dashed. So I think that that's going to

be a really issue. Also, we all know

that the AI productivity boom is going

to be disinflationary, but again, we're

slow. Microsoft, as I mentioned earlier,

they haven't been getting that uptick in

those revenues just quite yet. So, I

think interest rates are going to be

where it's at. And that slowness to see

the dis disinflationary effects. And

plus, just this week, I got to buy a new

laptop for my daughter. I'm wealthy. I

could pay 200 bucks, 300 bucks more. But

you look at the average consumer trying

to buy a new computer for the kid to go

to college and they get a 20% hike

because, you know, Micron is in an

earnings bubble. I think that's really

going to start weighing on people by end

of year.

>> Lee, why don't you buy me one while

you're at it? I mean, come on. You got a

couple bucks.

Interactive Summary

Ask follow-up questions or revisit key timestamps.

The video discusses the state of the market exiting the second quarter, highlighting strong gains in the S&P 500 and NASDAQ driven by AI investments. Experts analyze the sustainability of this growth, questioning whether the "Mag 7" can translate heavy capital expenditure into actual productivity and profits. Furthermore, the discussion touches on the "K-shaped" economy, where high-income households drive market growth through wealth effects, while lower-income segments face rising costs for goods and services, alongside concerns regarding interest rates and the potential risks of the AI trade failing to yield broad-based economic benefits.

Suggested questions

3 ready-made promptsRecently Distilled

Videos recently processed by our community