The First Great Depression: Lessons from the 1873 Global Financial Collapse | Liaquat Ahamed

Now Playing

The First Great Depression: Lessons from the 1873 Global Financial Collapse | Liaquat Ahamed

Transcript

1127 segments

In the middle of a financial crisis,

everyone tries to hoard precious metals

and get out of paper money. You draw any

chart of default rates on US corporate

investment and it is the highest in our

history. It wouldn't surprise me if we

got a series of mini booms and busts on

in the AI boom. Every private sector

infrastructure boom faces these issues

where the collective consequences of of

these competitive attempts to become

number one lead to poor returns for

everyone and at some point that's going

to kick in. I am so glad today we have a

very special guest, one of my favorite

authors of all time, Lea Ahmed, who's

the author of the new book 1873, the

Rothschilds, the first great depression

and the making of the modern world.

Leaquat, welcome to Monetary Matters.

>> Thank you, Jack, and thank you for

having me.

>> I want to ask you about 1873,

why it's so important, what drew you to

this year? I had written a book about

the leadup to 1929 and the Great

Depression and that focused very much on

the conduct of monetary policy by the

four central bankers. And I was looking

around for another financial crisis. I'm

I'm actually not a misenthrop, but I do

I do like writing about financial crisis

because as an economic historian,

they're really quite dramatic and

history speeds up and lots of things

happen. And 1873

really piqued my interest because it was

both a giant financial crisis or

sequence of financial crisis in three

different financial centers

but superimposed upon it was a crazy

reordering of the monetary system and a

totally unnecessary reordering of the

monetary system that very few people

seek to know about. I thought that makes

a fantastic story of, you know, both

what a boom bust cycle looks like and

then throw in a sequence of major

monetary missteps. And since 19 since my

original book, the Lords of Finance

argued that the central

mistake in in the 20s was a series of

monetary policy mistakes. I thought this

this sounds just perfect material for

me.

>> Yeah. Your book Lords of Finance 19

about the 1920s and 1930s in my opinion

the greatest financial history history

book in in in my opinion. Um

>> tell us what was the monetary misstep

coming up into 1873.

>> Okay. For 50 years, the world had relied

on a combination of gold and silver as

the foundation for the mum tree system.

And we'd had periods of major gold

discoveries and we'd had periods of

major silver discoveries.

And it had proved the system had proved

to be really quite resilient.

uh that when uh when there was a lot of

silver the that was absorbed by central

banker banks and when there was a lot of

gold that was also absorbed by central

banks. So the monetary base if you like

which depended on precious metals was

really quite stable and grew quite quite

systematically.

And at the heart of this were two

countries somewhat surprisingly

the US which depended which relied both

on silver and gold and France which also

had a bi metallic system relying on gold

and silver.

Now half the or or I don't know a third

of the world a third of the financial

world the Britain was on gold the other

third was on silver so Germany China

India Turkey Mexico you know were all

based on silver and the the swing factor

and and that acted as a sort of

balancing uh balancing item

uh was was France and and the US and it

had worked brilliantly. We'd had stable

prices throughout the 19th century

and in 1873

and this is not a well-known story.

Bismar had defeated France on the

battlefield

and decided to double down

by trying to attack France

using his uh his reserves, his his

precious metal reserves by dumping all

his silver and moving to gold in the

period of 1 to two years,

thinking that that way because the

French held the most amount of silver in

the world that they he would be damaging

France and

and he did but he damaged himself. It

was actually a self-inflicted wound

because every country in Europe at that

point panicked and started dumping their

silver and that caused a giant sort of

move from silver to gold and people

started trying to hoard central banks

started trying to there was a scramble

for gold and under any sort of precious

metal standard whenever everyone tries

to scramble for a particular precious

metal. It causes a contraction in in

liquidity and money supply.

>> So Bismar, the head of Germany, won a

war against France and wanted to

penalize France. So moved off of silver.

Why did that cause a contraction in

liquidity? And also what years is it?

This is before 1873 or exactly 1873. it

actually exactly in 1873

>> and the world could have coped with it

if you know under normal circumstances

but to do this in the middle of a

financial crisis. Now, anyone who knows

about financial crisis crisis knows that

in the middle of a financial crisis,

everyone tries to hoard precious metals

and get out of paper money. And so the

role of the central banker banks is to

expand their money supply and

accommodate that demand.

And uh to have that occur, to have

Bismar try to damage France and cause it

to contract its money supply right in

the middle of the financial crisis was a

step too far.

And the most visible sign obviously was

what happened to wholesale prices. So if

you track silver prices versus gold and

they exactly match year by year what

happened to commodity prices and that is

the single most important determinant of

what caused the deflation from 1873 to

the 1890s.

>> And all of the countries kind of decided

to go off silver and gold together. So

they just go to to gold or was it kind

of peace meal and you know first it was

France then it was the other ones as

well.

>> Okay. There was a conference in 1867

where there was a pie in the sky plan

with the idea that everyone should move

from silver and gold to gold. Now this

was 1867.

The world was experiencing a major

expansion in gold supply after the gold

discoveries of the 1840s and 50s. The

world was booming.

So it it was a perfect environment.

The only people who refused to sign up

for this

were Britain and France.

So it was a plan that never went

anywhere.

>> Okay. and essentially was a non-plan and

maybe it would have been a good idea if

there hadn't been an intervening

financial crisis in 1873.

All showed complicating the fact the the

the situation was that gold discoveries

slowed down dramatically.

So the you know the hope had been we'll

all move to gold because there'll be

enough gold in the world to sustain all

of us. But you know gold discoveries are

a random affair. And you know unluckily

this the new discoveries slowed down

dramatically

and only revived in the 1890s.

So, we're hinting at the bust, the

collapse of the financial system, the

the retrenchment. Let's talk about the

boom, though. Did the boom begin in the

late 1860s or what what caused this the

huge surge in investment and and growth

and and the bull market of the late60s

early 70s.

>> Okay. The bull market had started in in

1850

and it had been fueled by a massive

expansion in the bond market and the

architects of that expansion in the bond

market were the Rothschilds. Hence

that's why they appear in the title. It

was actually a totally rational boom

there. You know there were new

opportunities.

The supply of savings from the two major

savers in the world which is Britain and

France was steadily expanding and the

expansion in the bond market essentially

channeled those savings into massive

infrastructure projects around the

world. So the railroads, ports, you

know, the laying of the undersea cable,

communications.

Um, and it was a it was actually a

really quite benign boom, uh, with, you

know, no excesses.

In 1870,

as the boom was sort of breaching its 20

year mark, France and Germany went to

war. I mean France was the second

largest capital market in the world, the

third largest economy. Paris was

surrounded by Prussian troops, was

starved into submission at the Paris

Stock Exchange was closed for months and

everyone thought, God this, you know,

assumed this would be the end of the

boom.

Instead, the disruptions to capital

flows

fuel

in the perverse way that financial

markets always disabuse of everyone of

their expectation

fueled a series of bubbles and the

bubbles were three-fold. One, the money

that Germany got from France fueled a

stock market bubble in Berlin and

Vienna.

Secondly, a lot of capital went into the

US which was immune from European wars

and gave an extra boost to the railroad

construction boom which had been going

very steadily but suddenly in 1870 took

a giant leap forward. And thirdly, the

it converted the UK the the London stock

exchange into a giant casino

where all sorts of small companies and

new borrowers from sovereign countries

were able to float bonds and were able

to float stocks and bonds and there was

a speculative bubble on the London Stock

Exchange. So you got three simultaneous

bubbles and totally unforcable

in in the space of the three years from

1870 to 73.

And so those three bubbles were the

stock exchange in London, the real

estate and stock market in Berlin and

Austria and then the US railway boom.

The the railway boom was a lot bond

funded, debt funded, not equity funded.

So, Leaqua, what was was there a cause

or a series of cause that propelled

these three bubbles at the same time or

did they have different causes?

>> France having to pay a billion dollars

to Germany. And by the way, a billion

dollars converted today to today's money

adjusted for the size of economies would

be about 1.2 1.3 trillion.

>> Wow. And you'd assume that, you know,

$1.3 trillion

going from the hands of savers in France

into Germany where the money gets spent.

You can understand why it caused a

bubble in Germany. Why it caused these

other little bubbles which were just as

significant.

And suddenly you know railroad bonds

which had been running at you know I

don't know 2 3% of GDP

boo suddenly boosted to f four five 6%

of GDP in the US and foreign sovereign

debt issued on the London stock exchange

which had also been running at 2003 $300

million a year suddenly jumped to $500

million. I don't think anyone fully

understands that

sometimes, you know, you can get these

situations where you get when sources of

savings

suddenly get unleashed, everyone looks

around and says, "Who knew there was so

much money sitting on the sidelines?"

>> Yeah.

>> And I think that's what happened with

the FrancoRussian War.

>> Okay. So when So let's say so when did

things really start to get hot? 1870

1871.

>> Yeah. 7172.

I mean truly hot and and you know

everyone was predicting by by by the end

of 1872

people were predicting disaster

certainly in in Berlin and Vienna but

they were also predicting you know

people were complaining about how many

railroads were trying to raise capital

in the US and you know the economist was

railing on about all of these all of

these countries coming to borrow on the

London Stock Exchange and people buying

their bonds who knew nothing about these

countries. And I in my book I focus on

two in particular

Egypt and Turkey which borrowed the

equivalent of $1.5 billion

which was is was actually I mean just to

give you an example

if $3 billion went into the US railroad

boom

about a billion came from Europe.

The idea that savers in Europe should

devote $1.5 billion dollars, 50% more

than they devoted to to American

railroads to financing Turkey and Egypt

is just sort of mindboggling.

>> Yes. And the the the return of

investment on these bonds

doesn't seem to me to be a particularly

good investment. Then we you know as as

we said before that a lot of this money

was invested with what we call what's

called retail investors in fixed income

and bonds rather than equities. Like

today people may be buying stocks but

back in the day they would be buying

bonds. And it just seems to me like if

you invested in the equity of a railway

company, you know, you're probably going

to lose all your money, but if you don't

lose your money, it could 5x, it could

10x, but it seems like because when

you're lending to a railroad at 10%,

your upside is capped and you you have

all these risks. It doesn't seem to me

to be a particularly good investment,

nor does it seem to me to be a

particularly good investment to lend it

to these bankrupt monarchs of of Egypt

and Turkey. Did that occur to investors

at the time? Did it occur to them later?

Well, I think it occurred to them later

that

at the time people had uh certainly in

um stock investments, so equity

investments

had developed a very bad name in 18 the

mid the late 1840s and 50s.

>> Why?

>> Uh because uh of two main factors.

One was there was a railroad mania in

Britain

uh where railroad stocks went up 3x 4x

on average and then collapsed

and people got themselves very badly

burnt.

So so that was that was the first

factor. The second was that the largest

bare market of the 19th century

occurred from 1848

onwards. 18 maybe 1847

and it was essentially because you had

revolutions

>> throughout Europe and they you know

people had seen that they thought the

you know the French government was going

to fall. There were revolutions in every

country and it caused a you know total

disruption in capital markets and people

expected to lose all their money.

superimposed upon this a book had been

written by Charles McKay, the famous

book about manas and bubbles and it sort

of reminded everyone that periodically

investors totally lose lose their minds

and invest in crazy things. So the

combination of these three things led

people to say you know we should just we

you know we led the middle class and

there weren't institutional investors at

the time.

that this was fueled by a rising middle

class, two three 400,000 people spread

across Britain, France, Germany, and the

US who were just getting to the stage

where they could start accumulating

significant amounts of money and they

thought we're going to put it all into

bonds. The dilemma was that as they

started putting it into government

bonds, government bond yields went down

to two 3%.

Uh you could get 3% in the UK, you could

get 4% in the US

and suddenly the railroads appeared and

were offering 8 9%.

and fly by night borrowers from Turkey

and Egypt were offering 9 10%.

And people were not experienced enough

to realize that these guy these gains

are totally elusory

or the these returns are potentially

totally elusory. So people put vast

amounts of their net worth into into

these bots. You know just uh to give you

an example the the British prime

minister Gladston put a 40% of his net

worth

into Egyptian bonds.

Now you know luckily for him he was

governing British policy towards Egypt

so he could determine the outcome but

for most people they weren't in that

situation. So, so equities had a bad

reputation, people were plowing money

into bonds and I also think that because

inflation was low and we'll see later

negative like earning 8% in nominal

terms and then getting 10% in real terms

because deflation it's not it's you know

not a not a horrible prospect and then

also did you have this thing of kind of

like private credit of you go to the

bond market and and you buy from the

Rothschilds or someone who bought from

the Rothschilds and then you park it

away you tuck it in your drawer and you

feel good about it, you're not, you

know, if you're a a middle- class saver,

you're going to work, you're not like

checking, you're not going to the

exchange every day to see the price.

>> No. Yeah. Exactly. This, you know, this

was supposed to be giving you a coupon

every year and, you know, was going to

sustain put your kids through school

and, you know, sustain your middle class

life. Tell me about the railway boom.

When was it rational? When did it be

become excessive? I think it was

rational until 1870.

You know, it was running at about in

both the US and and Europe, it was

running at 4 5,000 miles of construction

a year. The returns were reasonable.

The transcontinent the first

transcontinental railroad

was completed in 1869.

in 1870

a series or in it's actually in 1872 but

sort of between 1870 and 1872

it be it began to be apparent that many

railroads had been constructed

way in advance of demand.

So returns on on railroad bonds, returns

on railroad investments had gone down.

Now they were meeting their their

dividends by continuing to borrow. But

there were clearly signs of excess

investment in in US railroads.

In the 18 in 1872,

a series of scandals

roughed the railroad business and in

particular was revealed

that the first transcontinental railroad

which had cost $70 million.

Of that,

$30 million had come from government

subsidies in the form of land grants and

cheap lending through the state.

On top of which

costs have been giantly inflated

because the railroad companies had

discovered this Whis where the the

sponsors of the railroad companies would

create created a private company which

would do the construction and the

railroad would subcontract to the to the

private construction company to actually

construct the railroads.

And the most famous was a company called

Credit Mobilier, which all sounds very

sophisticated and they borrowed the the

French name from a French bank, but it

was just a device

for siphoning excess profits from

railroad shareholders to this group of

insiders. And the people who were who

who ran the insiders,

one was a congressman O gains and he

started giving out shares

in or giving out equity in this in this

construction in credit mobilier

to favored congressmen.

It was the biggest corruption scandal

until then of the 19th century that

essentially

congressmen and politicians who were

responsible for licensing and allowing

the railroads to to expand were getting

were making themselves rich. When this

got revealed in 1872,

there was a wave of disgust

and the funding from Congress dried up.

So the second transcontinental railroad

which was which was a company called

Northern Pacific which was built which

was trying to construct a northern route

across the country and had hoped to be

able to get sub the similar subsidies

from Congress suddenly found its sources

of money drying up

and in 1873 it ran out of funds.

And at that that's what precipitated the

collapse of the railroad the first

railroad bubble.

>> How many people lost a lot of money in

this? And can you give us a sense of the

scale of the losses that investors

experienced perhaps in in the United

States and also I we can compare the

railroad investment capex from railroads

as a percentage of GDP. you know in

1850s it was like 3% then it it dipped

down and then as you said in 1870 it

exploded higher to 4% 5% of GDP later we

can compare this to the data center boom

we have now I think data center as a

investment as a percentage of GDP in the

US is around 2% so it's below the

excess's peak of of railroad so it it

could get if it you know could get as

crazy as 1870 could get even crazier but

just I want to get a sense of the the

losses and and precisely,

you know, do do you think that it's

almost guaranteed anytime you have a

capital expenditure boom that they're

going to be excesses that lead to

losses?

>> Well, let me describe the numbers first.

So, the 1870 boom by 1873

the outstanding stock of Oh, great great

graph.

By by 1873

the outstanding stock of railroad bonds

was two to two and a half billion issued

in the US. Over the when when after the

crash came

half the railroad companies in the

country went under and stopped paying

interest. So over a period of 3 four

years the the volume of of defaults was

roughly 50%.

>> Volume of default of 50%. That is so

high.

>> I mean it's the it's you know you draw

any chart of default rates on on you

know US corporate investment and it is

the highest in our history.

uh now not you know that that doesn't

mean you you got zero dollars back so

50% and let's say you got

3040 cents of your money back so the

total losses were somewhere between 500

million and a billion dollars so in a

country where the GDP was running at$8

billion dollars you know That's 10% of

GDP over a you know so let's say 2 3% of

GDP over a period of four years. So that

gives you the scale of the magnitude of

the losses. So what were we? Yeah. So

that was that and that I think what what

people were re somewhat reassured

was that this was essentially the

equivalent of high netw worth

individuals.

I mean this was not you know your

average person your average man in the

street. This was, you know, people who

bought railroad bonds had money to

invest

and they and they had the ability to sit

through losses. I suppose a bit like

private credit today. So, so it didn't

it didn't translate into a giant

collapse in spending

to give you an idea of the other bubbles

in the world.

So the the European stock the central

European stock market bubble

essentially caused equities to go up

about a billion dollars went into

equities

and the stock market collapsed by 70%.

So we got and these were these were

actually not high netw worth

individuals. So they were, you know,

they were the man in the street who got

caught up in in the mania. Well, not

only the man in the street, princes and

duchesses and everyone got caught up. So

this total losses in central Europe were

a few hundred million dollars.

And then if you take the emerging market

debt boom,

if you count how much went into emerging

market debt, about $2 billion went into

emerging market debt.

And let's say half of that went uh was

never paid back. I mean, Turkey, a

billion dollars went into Turkey and

essentially they were forgiven half of

that. and then you know rescheduled the

other half. So you essentially got 25

cents

on on the dollar of your money back. So

that gives you an all sort of sense of

magnitude of of all of the losses around

the world.

>> What were the lessons learned from 1873?

What did what did you learn? What what

can you what can we draw from this?

>> Okay. Well, I mean I I make a big deal,

I suppose, because of my own interest.

of you know this crazy remaking of the

monetary system. The boom bust cycle was

not great and it you know it caused a

recession. Compounding the losses was

the deflation that followed where prices

fell over the first five years by 25%

and then over the 20 years by a total of

40%.

Now there is nothing worse

than having a you know as we found out

in Jer Japan there is nothing worse than

this sort of insidious deflation where

prices keep falling and it causes

massive

uh

redistribution of income

from debtors.

So debtors found themselves belleaguered

for 20 years. Now some of these were

farmers in the in in the west or they

were junkers, you know, the Prussian

aristocrats,

but some of them were just businessmen

and you got got a reaction where

everyone tried to get the government to

to help them out. So you got a wave of

protectionism.

uh you got you know Europe had been

moving towards free trade

and you suddenly got uh a jump in

protectionism in Europe. Germany. Bismar

who had sided with the liberals in favor

of free trade changed changed the party

he supported to the conservatives and

supported the the right-wing party which

was in favor of agricultural protection.

So we got a jump a jump in agricultural

protection essentially designed to save

Prussian aristocrats

and across Europe the the move towards

free trade uh docked. So not very

different from the sort of wave of

protectionism that we've had in the

world the last few years. The US was

already highly protectionist

but even it raised tariffs on

manufacturing.

So and it caused more than the economic

consequences

was the political fracturing.

You know, it it pitted

people who earned their money from the

land

against everyone else and was the single

most important factor in the wave of

populism in the in the US. uh was uh

created giant problems across Europe

including for you know aris British

aristocrats

who had to get rid of their estates

wholesale. I think there was a I I cite

a statistic where of a hundred British

aristocrats

some astounding number married off their

daughters to American millionaires.

So it, you know, it caused a major

social disruption

>> because agricultural prices went down

and and part of this was monetary as you

said. I think a part of it was the rise

of the steam ship. So actually I think

in in Downtown Abbey I think the uh you

know Robert the the Lord Lord Granthm is

he's married to an American woman who's

like an American millionaire a ays and

as people who have seen the show know

that you know he's having some financial

troubles. because it's, you know,

running an estate is not a great

business from the years 1870 to 1920 in

part because of the the demonetization

of silver as well as the steamship. And

I think literally I think actually

Kora's dad was a a steamship guy, unless

I'm confusing with someone else from

from your book. I could get

>> No, you you know he by the way down

everyone's seen the house from Downtown

Abbey.

I'm assuming that belonged

to the do a Rothschild daughter

>> really.

>> So and by the way the Rothschilds had 41

such estates across France and Britain.

So you know it gives you a scale

an insight into the scale of the

Rothschild wealth. She was the daughter.

She was her father was actually gay and

but had a mistress.

>> Is this Adulus? Adulus or Nathaniel?

>> No.

God, you're confusing me now.

>> Oh, sorry. Don't worry.

But his daughter married the Earl of

Carnavvern

and she and the Earl of Carnavvern

first of all financed

the the attempt to find two

>> Alfred. Alfred

>> Alfred. Yes,

>> I told you I read the book.

>> Right. So Al Alfred was a real character

because he was gay and very flamboyant

and was known throughout London, but he

did have this mistress and he did have

this illegitimate daughter and she was a

you know she was a sort of nasty piece

of work because she milked him from all

for all the money and the rest of his

family were very upset that she ended up

inheriting all of his Rothschild's mill

millions. But it did go into into

good causes, I suppose. And that that

house just stands as this total symbol

of the Rothschild wealth.

>> Wow. I I know that house was from the

Rothschild. So Leo, I just want to say

the book is fantastic. 1873. People

should buy it. I think they people who

follow my work and are a regular

listener who are interested in this

financial crisis, monetary policy, booms

and busts, they they definitely will be

entertained, find a lot of value as I

did and they also check check out your

original book lords of finance which I

as I said is a truly exceptional book.

Leo Lewat, what do you think after

having written this book and preparing

for this book for many years focusing on

the railway boom when in capital

expenditure as a percent of GDP reached

as high as five five a.5%. What do you

see think now as you watch the global

data center AI boom where literally I

mean just I think in the US a trillion

dollars this year is going to be spent

on on AI data centers certainly that

much if you count other countries as

well what are your thoughts how much of

a comparison are can we draw

>> okay so look it a trillion dollars is

probably you know 3% of GDP it is a

global boost

So it's not just in the US that you know

it's being financed and underlying it

are all sorts of electrical and

infrastructure companies based in Europe

based uh chip companies based in Taiwan

and um and Korea.

So the world is a very large place.

Global GDP is whatever a hundred

trillion dollars. uh US is $30 trillion.

So we could we can finance several years

of a trillion dollar investment boom.

So I don't think the problem is going to

be a supply constraint on finance.

The only problem will be a that they are

all competing with each other.

All of these companies building and they

all want to be number one and the

returns for being number two or number

three may fall dramatically short of

expected returns and it's not clear

that the AI companies have developed a

business model for generating re

revenues on the trillions of dollars

they're going to invest. So it's just

every private sector infrastructure boom

faces these issues where the collective

uh consequences of of these competitive

attempts to become number one lead to

poor returns for everyone and at some

point that's going to kick in.

Now the lesson from the railroad boom

was we got a bust in 73 which lasted for

5 years.

We then got another boom in the early

1880s.

More equity financed, less debt. So they

they'd learned one lesson.

And then we got another bust and we got

a third mini boom in the 1890s.

So the railroads transformed this

country, but they didn't do it in one

fell swoop. And there were several booms

and busts along the way. And it wouldn't

surprise me if we got a series of many

booms and busts on the in the AI boom.

It did strike me reading the book that

throughout the late 19th century the bus

the the recessions depressions lasted so

long three years five years as you said

it almost feels like policy makers now

particularly in the US consider it

illegal to have a recession and if if

there's a you know a market panic and a

bare market and financial conditions

tighten they're not doing their job if

they don't aggressively try and mitigate

those conditions unlike you know we had

the so-called free market in in in the

late 19th century. Your thoughts there

here?

>> So the I I think it was product of two

things. One is governments did not think

it was their responsible to smooth out

the business cycle.

But secondly, and then I go keep going

back to my whole thing of the monetary

environment.

There was just not enough money around.

And I I I liken the economy of the late

19th century

to trying to drive a a car with your

foot on the brake and your foot on the

accelerator and the other foot on the

brake at the same time that it was a

series of stopgo

cycles

and we got you know we we it was I mean

it it was 2 and a half% growth for that

20 year period. So that's great, but it

occurred in in fits and starts.

And if you have a monetary environment

that is way too tight,

that's what you're going to get.

Now, we're about, you know, we learned

that lesson.

Maybe we're gonna make a totally

separate mistake, which is we're gonna

be too loose going forward and we are

we're going to have to live with as

opposed to the deflation of the late

19th century. We're going to end up with

systematic inflation

of the 2020s onwards. and the, you know,

being a bond investor is not going to be

a good place to be uh because interest

rates are going to constantly be spiking

up. So, you know, I can envisage all

sorts of scenarios.

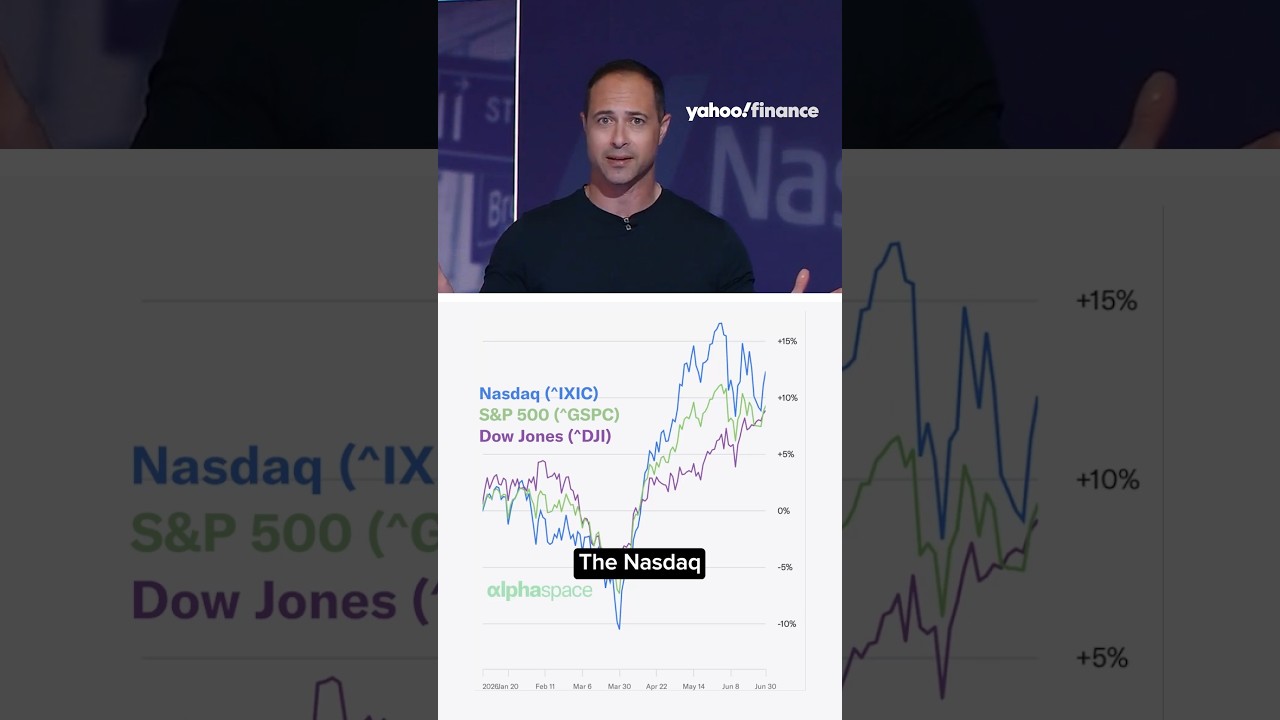

I history is not going to repeat itself.

In in in a a piece where you were

interviewing in fortune, you you cited

the quote, "Things take much longer to

happen than you imagine, and once they

happen, they happen much quicker." As an

observer of financial history, tell us

how you've seen that throughout history.

>> That adage was was coined by Rudy

Dawnbush, who's a famous MIT economist.

I think he drew it from a quote from

Hemingway where someone asked someone,

"How did you go bankrupt?" And he said,

"Slowly at first and then very quickly."

So, so look that's if you draw business

cycles,

if you draw a chart of business cycles,

they are not they don't look like

cycles. They don't look like sign

curves. If you draw a chart of of the

stock market,

bull markets last a long time and climb

a wall of worry. Bare markets occur in

18 months, two years,

max three years. So you've got you get

10 years of a bull market

and then three years of a bare market.

So I think that is in a chart just just

that chart would summarize would

summarize the the Rudy Dawnbush adage

very well. I wonder you you have a piece

out in the in the Times about the AI

boom and how it's global, not just in

the US. What motivated you to write that

piece?

>> I mean, one of the characteristics of

both my books and all of my thinking

is that in the US, we have a tendency

to be somewhat parochial

about

markets. what's happening in the world

and we exaggerate you know our own

influence

and we don't pay enough attention

to the fact that we are just one element

of the global economy.

So Lords of finance you know essentially

argued that you couldn't understand the

great depression if you just focused on

the US. You had to see it in the full

context of what was going on in Europe.

This book 1873

sort of argues that point in spades

because the US at that point was only

one among four roughly equal economic

powers.

Now we are now, you know, a $30 trillion

economy

and it, you know, we're able, we have a

$60 trillion plus equity market which

accounts for 65%

of the global equity market. So we're

able to

carry the illusion

that we we are the only act in town

and I'm just trying to argue the case

that there's a whole big world out there

and that you know we we have made maybe

we've become a little bit too seduced

by you know we've drunk our own Kool-Aid

and believe that uh the US is the only

place to invest and the last 18 months

is a reflection of that that we've had a

a a mini boom going on in the rest of

the world all driven by AI and AI may be

American in conception although even

there I would argue that many of the

people who came up with AI were British

but but the the execution ution and the

implementation of the AI boom is a

global phenomena and is going to tap

into a full range of global companies.

>> Yes, you've got some companies like

Nebius and ASML. In the Netherlands, in

Japan, you've got a lot of semiconductor

giants. In Taiwan, you have Taiwan

Semiconductor. In Korea, you have the

memory players.

All of those companies are in the Msei

World Index or the Msei XUS Global

Index. So you're absolutely right as you

point out that since the beginning of

2025 emerging markets generated returns

of 53% Europe 44% Japan 40% while the US

equity market is up considerably less. I

might just add that it is very

concentrated in global. It's like

Netherlands, Korea, Taiwan and Japan.

Other than and the US and then China.

But other than that, it seems like the U

the AI boom is

>> I don't know. French French construction

companies and German energy and you know

I think there's you know uh yeah I mean

I you probably know know these numbers

much better than I do but I I just get a

sense that we I this was actually almost

just a plea for a certain amount of

national modesty. I well I certainly

endorse that hardly. Yakquat, what

terrifies you about financial markets

now and what gives you hope?

>> Well, what terrifies me is some of the

crazy stuff that you see, you know, when

a sneaker company um I'm blanking on the

name, the

>> Yeah. can convert itself to an AI

company and see its stock go up, you

know, threefold. the fact that over the

last three two and a half years, you

know, we we've had these many

speculative bubbles

in crypto,

in gold, and silver.

There's something a little bit

overroought

about financial markets that is that

can, you know, I I just don't believe is

healthy.

and combine that with a handsoff central

bank that is clearly going to be under

political pressure to keep interest

rates low is makes me nervous

and you know reminds me of the late60s

early 7 1960s early 1970s.

So that particularly uh makes me

nervous. Now what gives me hope

is the sheer

innovative capability of you know we we

we've had these modest productivity

boomlets.

We had one in the late 1990s and we look

and you know you never know but we look

as if we're beginning to get one now and

there's every reason to hope that we

could be in for a a nice productivity

jump

associated with all of these new

innovations. Tell us, you said a bubble

in crypto, a little bubble in gold and

silver.

Wouldn't what what do you make of the

argument that gold and silver is

primarily rising because you you know

investors in China and India as well as

governments around the world are buying

it because they don't like the US

Treasury's debt position and they don't

like the US government kind of bullying

countries around such as what the the US

Treasury did to Russia. I'm not saying

Russia didn't deserve it. we kind of

canled like billions of of their money

of their money

>> that you know uh that's one more reason

to be scared.

>> Yeah. the geopolitics, the geopolitics.

And you know, look, you would be worried

if you had a central bank, the the US

central bank is not, you know, is not

essentially conveying a message

that don't worry, we've got it under

control. you know, we've exceeded our

inflation targets for, you know, the the

last five years, and it doesn't seem as

if we're in a hurry

to try to reassure everyone

that that we are we are going to meet

meet those inflation targets. So, you

know, that's another reason to to be

worried.

>> Tell us your thoughts about incoming Fed

Chair Kevin Worsh. He is likely to be a

little bit dovish. So lower interest

rates on interest rate policy, but a

little bit hawkish on balance sheet

policy. So he's stated his desire to

reduce the Federal Reserve's balance

sheet and role in the market. I've

actually got some exciting interviews

coming up on that topic with some of the

like best informed people on in the

world on that topic. But I wonder, Leo,

you've studied central banks policies

and policymakers actions towards gold,

towards silver, the demonetization of

silver in the 1870s, the move of central

banks back onto the gold standard during

the 1920s after the World War I. We

moved off of it and both those extremely

painful transitions forced on the

monetary system by the central bankers,

a tightening. I wonder are we at perhaps

a same juncture where the balance sheet

is going to be significantly reduced and

and do you view that as as comp

comparable or even similar at all? You

know, not really because I, you know, I

think

>> the central objective I I mean I I think

there probably ways to get the balance

sheet down

without putting pressure on interest

rates, but and it'll probably put

pressure on a little pressure on

long-term rates and compared to

short-term rates, but I find it very

difficult to see how he achieves leaves

I mean a certain amount of deregulation

uh will will clearly reduce the the

bank's needs for banks need for reserves

and therefore that they may be able to

get the balance sheet down but I find it

very difficult to see how he's going to

be able to reconcile his interest rate

objectives with his balance sheet

objectives

>> the book is 1873 the Roth child's the

first great depression and the making of

the modern world. People should go out

and buy it as soon as they're done

finishing this interview. Leaquat, thank

you so much.

>> Thank God.

>> Thank you. Just close the door.

Interactive Summary

Ask follow-up questions or revisit key timestamps.

The video features an interview with economic historian Liaquat Ahamed, author of '1873: The Rothschilds, the First Great Depression and the Making of the Modern World.' The discussion centers on the financial crisis of 1873, exploring its causes, such as the demonetization of silver, the bond-funded railway boom, and geopolitical conflicts. Ahamed compares these historical events to the current AI-driven infrastructure boom, noting that while there are similarities in competitive over-investment, today's global economy differs from the 19th-century gold and silver standards. The conversation also touches on the lessons regarding deflation, protectionism, and the potential risks of current monetary policy and geopolitical tensions.

Suggested questions

3 ready-made promptsRecently Distilled

Videos recently processed by our community