Why Big Banks Are Selling-Off | Prof G Markets

Now Playing

Why Big Banks Are Selling-Off | Prof G Markets

Transcript

833 segments

Today's number, 100. That's how many

body parts were stolen from cemeteries

by a man in Pennsylvania last week.

Authorities confirmed this after they

broke into his storage unit. When asked

what they found, the officer replied,

"Remains to be seen."

Welcome to Profy Markets. I'm Ed Nelson.

It is January 15th. Let's check in on

yesterday's market vitals. The major

indices all ended the day in the red for

a second day. The NASDAQ led those

declines dragged down by Nvidia after

Trump announced new security

requirements for H200 chip exports to

China. Bank stocks also fell following

their earnings. We will talk about that

in a second. Oil prices dropped after

President Trump signaled an attack on

Iran is not imminent. And finally, gold,

silver, and copper all hit record highs.

Okay, what else is happening?

Fourth quarter bank earnings delivered a

mixed picture, but Wall Street's verdict

on bank stocks was quite simple. Sell.

Cityroup fell 3%, Bank of America

dropped 4%. Wells Fargo slid 5%. That's

the most in 6 months. And JP Morgan fell

for a second day. It's down more than 5%

since its Tuesday earnings. Let's take a

look at the earnings themselves.

Cityroup beat estimates but saw profits

slide. Bank of America beat on revenue

and net income with quarterly profit

actually rising 12%. Wells Fargo

disappointed with its net interest

income. And JP Morgan topped

expectations. However, profits fell 7%

after a one-time hit tied to its Apple

Card deal. But mixed results weren't the

only thing weighing down these earnings

calls. Bank executives also had to

contend with fresh political pressure

after President Trump floated a proposal

to cap credit card interest rates at

10%. On top of that, the sector is still

reeling from the news about the DOJ's

investigation into Federal Reserve Chair

Jerome Pow. A lot here, a lot to unpack.

We are speaking with Saul Martinez, head

of US financials research at HSBC. Saul,

thank you very much for joining us on

Profy Markets.

>> Thanks for having me.

>> So, we want to get your reactions to

this earnings. We've seen earnings from

all the big banks here. Um, and

generally a sell-off. Uh, any initial

reactions?

>> Sure. No, I think the I think the

divergence between what were generally

good results and outlooks and negative

share reactions does is telling of high

expectations going into these results.

So I'd characterize these results as is

good not great. Now the in many respects

the results did really validate the

bullcase for banks. Net interest

income's growing, loan growth picking

up, capital markets revenues have been

good, credit quality is good. um they're

managing their costs effectively. The

expectations from the banks are that

profited levels will go up. Um as you

said though, I had the stocks reacted

negatively. JP Morgan down 5% since they

reported on uh yesterday and City, Bank

of America, Wells Fargo were all down 3

to 5%. Now I I think this, you know,

does reflect that the big banks have

become, you know, darlings. um they've

outperformed considerably

uh last year. They outperformed in 2024.

Valuations are historically elevated and

I think there's some disappointment that

results weren't even stronger. I think

that is reflected in the guidance. The

guidance that banks gave for 2026 is

pretty much in line with where analysts

are at and likely doesn't trigger uh

material upgrades from analysts. And if

you overlay concerns about policy, which

I I expect we'll we'll probably get into

with cards, it shifted sentiment a

little bit towards the bank. So, I think

it it's a reflection of of high

expectations coming in and the fact that

the results were good, but they weren't

great and they didn't ne and they're not

necessarily going to lead to lead

analysts and investors to really ramp up

their expectations, their baseline

expectations for earnings and

profitability going forward. Just

looking at some of these businesses, I

mean, Wealth Management um was a success

at Croup, Bank of America, Wells Fargo.

>> Um some really impressive M&A numbers

from from Croup 84% record deal making.

>> I'm just thinking about what Wall Street

is expecting or what they wanted in 2026

and what they didn't get in that

guidance. Is there a story that they

that you think that Wall Street was

expecting perhaps to do with uh

investment banking revenue, perhaps to

do with maybe the IPO market? What do

you think they wanted that they didn't

see?

>> I think it varies a little bit by bank.

You know, some of the elements of the

results were good. Um but again like the

you know the out the expectation what is

in the market consensus is that capital

markets revenues will be strong, wealth

management will be strong. Um there is

an expectation

that we may be entering into a super

cycle of investment banking activity. So

I don't think folks are concerned about

investment banking or capital markets

related businesses. I think to a large

degree though there's probably some you

know some disappointment with net

interest income. So the traditional

business of banks um lending investing

in securities and what part of the bull

case for banks is that you're we're now

living in an environment where there's

positive real rates across the curve.

So, a lot of the loans uh and

investments and securities that banks

made in a low interest rate environment

are effectively repricing to a higher

interest rate environment. And you're

getting a positive benefit on asset

yields that's shriving net interest

income. And I think the expectation was

that banks would be even more positive

on net interest income. JP Morgan um is

you know gave some guidance in December

about net interest income growing 30%. I

think there was some hope that maybe

they would increase that. I think the

same story applies to Wells Fargo and

Bank of America. So I think there there

was some hope that the traditional

revenue driver of banks uh that

interesting would actually be a little

bit better than it actually was. But

banks are are basically saying that what

analysts are expecting from that from um

for revenues is is probably just about

right. And I think there was some hope

that they would raise guidance and and

and that would um you know lead to

higher earnings estimates going forward.

>> Yeah. Something that we should also

bring up, certainly putting pressure on

these stocks, um Trump's proposal to put

a 10% cap on interest rates on credit

cards, which the banks do not like.

Wells Fargo didn't like it. City didn't

like it.

>> Uh JP Morgan CFO said everything is on

the table to push back against this

proposal. Can you tell us a little bit

more about the proposal, how it will

affect these companies and if these

companies should really be worried about

it?

>> Yeah. Um, well, well, first of all,

there's a lot to unpack here and there's

a lot of uncertainties. You know, right

now it's a social media post as opposed

to a an actual proposal. You know, and

there's some questions about how it

could even be implemented. I think most

policy analysts, legal, uh, legal

analysts would tell you it requires

legislation. It's it's very hard to see

legislation passing on this uh by

January 20th. And it's it's hard to see

legislation passing that would implement

a cap of 10%. And um an executive order

on this would likely be met by with

legal action. Um so how this would be

implemented is is a very big question.

It would have a devastating effect on

credit the credit card business though.

uh a 10% interest rate cap on lending um

would make you know uh large swans of

the credit card business unprofitable.

Broad swans of the population would lose

access to credit. Banks cannot make

money and credit card companies cannot

make money given the loss rates on

credit cards with an in with a 10%

interest rate and there would be you

know so you would have to see a material

change to the business models. Rewards

would be cut. you would see more late

fees and it you know for JP Morgan and

Croup they would be affected right these

are important business for them it would

have a material impact on earnings but

you know especially for more pure play

credit card companies who do have more

exposure to riskier segments of the

population somebody like a Capital One

it would be you know fairly devastating

impact on their earnings and

profitability I think that if I make one

additional point though because I think

it ties into what we were talking about

earlier about you know the bull case for

banks and what's in the expectations of

the market. And you know, part of what

has made the banks, you know, so

attractive to investors is the view that

they're primary beneficiaries of

deregulation that Paul the the direction

of travel on policy is a good one.

You're going to see, you know, capital

requirements cut, less stringent

enforcement from regulators. And I think

this was a reminder that policy can cut

both ways. it's not a one-way track to

um you know easier, more favorable

regulation. And so this really threw

cold water on on an important part of

the bank uh bull thesis. And I think it

was a reminder that you know there are

risks and this is something we did

highlight in the report very recently as

one of the key risks for 2026

especially as we head into the midterm

election. And if you know if you do get

a situation where Democrats do really

well in the midterm elections, investors

will be you know we'll start to look to

2028 and it will be a reminder that

maybe the the the very favorable

regulatory policy that you've seen may

not always be that way. But we got that

reminder I think a little bit earlier

than expected with um with the social

media post last Friday.

>> 100%. It is fascinating the extent to

which Trump is influencing everything

including the markets and the businesses

of these businesses. I mean

as you say it's like it was all about

deregulation. That was the idea and then

that and that's what the the market was

getting excited about. Now it appears

that maybe the banks aren't friends with

the White House. Who knows? But the

point being this is what is moving the

market. This is what decides the whole

the whole game. Just before we end here,

I I I'd love to hear what we learned

from the banks about Trump's

investigation or the DOJ's investigation

into Jerome Powell. We were discussing

this earlier on in in the week and one

of our guests said, you know, it'll be

very interesting to see what these

titans of finance, what these leaders

say about one of the most cataclysmic

events that we've seen when it comes to

the Federal Reserve in the past few

years. What did we hear from from the

CEOs? Did they speak about it?

>> Yeah, I mean it it wasn't a topic of

conversation that was um you know front

and center. It it I think it did come up

in and in in um the JP Morgan earnings

call. I think the view of the banks and

I think Jamie did express this was

central bank independent is is important

and it's important for you know for you

know pretty obvious reasons. Um uh so I

I think banks you know bank CEOs you

know you know will express that that

view. I think, you know, I think it is

fair to say that, you know, bank uh CEOs

have to be, you know, they represent the

bank and they have to be, you know,

pretty um you know, they have to be, you

know, um very judicious with what they

say and how they say it and and but in

the current, you know, political

environment. But I think they did

express the view and they will express

the view that um you know central bank

is independence is an important part and

having those safeguards you know are you

know are important to important for the

US economy and important for um you know

um the central bank's ability to um you

know to carry out its mission of of

maintaining inflation under control. So,

you know, but I don't think we

necessarily learned anything or, you

know, bank CEOs, you know, stuck their

necks out in one direction or another

during the during their news falls.

Okay. Saul Martinez, head of US

Financials research at HSBC.

Saul, really appreciate your time.

>> Yeah, anytime.

>> We'll be right back. And if you're

enjoying the show so far, be sure to

like and subscribe to the Prof Pod

YouTube channel at the link below.

Support

for the show comes from Monarch. We've

all been there. You talk yourself into

an impulse purchase and then you spend

the next few weeks avoiding eye contact

with your bank statement. Let this be

the year where your money works with

you, not against you. And you can do

that with Monarch. Monarch is the

all-in-one personal finance tool

designed to make your life easier.

That's because unlike most other

personal finance apps, Monarch is built

to make you proactive, not just

reactive. And now with AI tools, Monarch

can comb through the data to surface

insights personalized to you, such as

hidden patterns, identifying lifestyle

creep versus inflation, changes in

savings rates, and more. This new year,

achieve your financial goals for good.

Monarch is the all-in-one tool that

makes proactive money management simple

all year long. Use code markets at

monarch.com for half off your first

year. That is 50% off your first year at

monarch.com with code markets.

We're back with property markets.

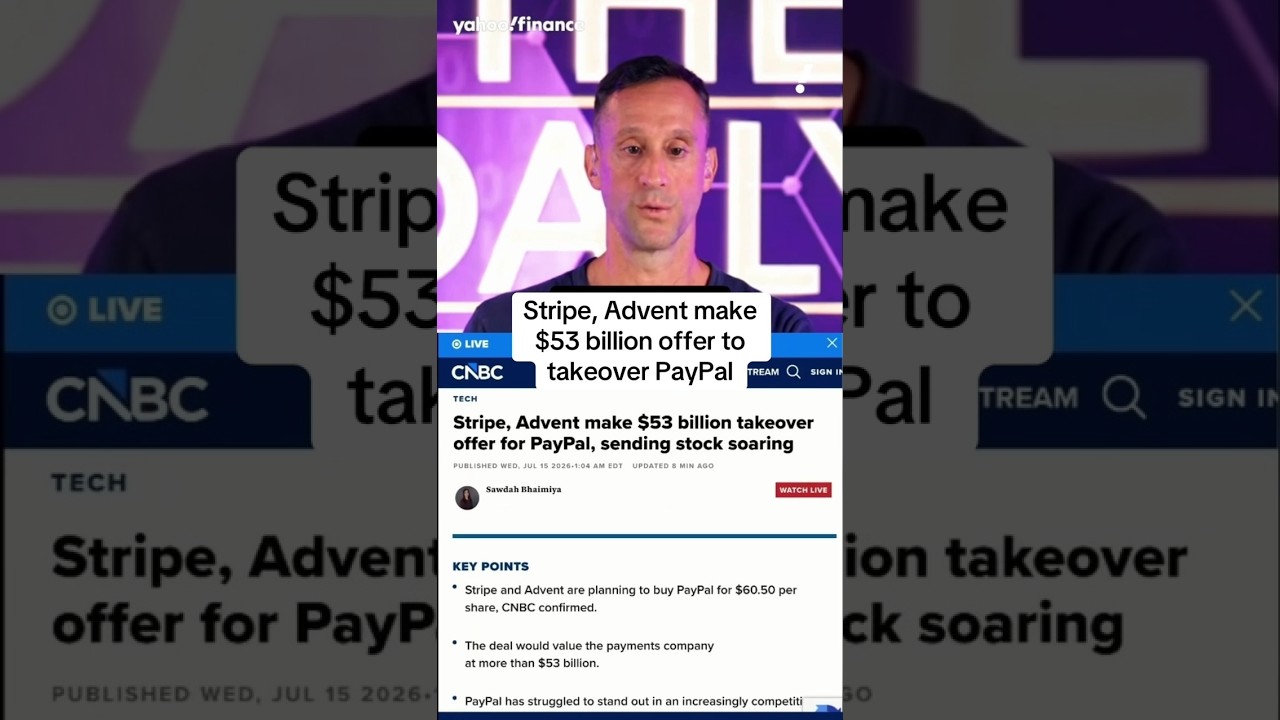

Netflix is reportedly preparing an

allcash bid for Warner Brothers

Discovery as the company moves to

fasttrack a potential sale. This news

comes shortly after rival bidder

Paramount launched a proxy fight on

Monday. The company is also suing Warner

Brothers Discovery and its CEO David

Zazloff for failing to disclose

information about its sales process.

Netflix and Warner Brothers and

Paramount Stock all closed down on this

news. Here to give us the scoop on the

state of Warner Brothers Discovery's

bidding war. We are speaking with Rohan

Gwami, business reporter at Sema and

Rohan actually has some new scoop that

he has just reported. Rohan, welcome

back to property markets. Ed, great to

be back with you. Hope you've been doing

well since we've last spoken.

>> Absolutely. And we do want to get an

update since we last spoke. I mean, last

time we spoke, we saw that Warner

Brothers Discovery had told its

shareholders to reject the Paramount

bid. They were encouraging shareholders

to go with Netflix. That was three weeks

ago. We're going to hear about your

scoop, but just before that, can we just

get an update on what has happened since

we last spoke in these past three weeks?

Yeah, you know, setting the scene uh in

the last three weeks somehow uh

Paramount came back again and said,

"Look, we've made some changes. We've

made our money a little bit more

certain." Like you and I talked about,

remember I I we had talked about how

their money wasn't totally short up.

Jared Kushner had just left. There were

some concerns about the sovereign wealth

funds. So, uh Larry Ellison, right,

David Ellison's old man, actually

stepped in and personally guaranteed uh

$40 billion, a huge portion of this of

this check. and and basically said, "I'm

good for it. I'm here for it. It it

really must be wonderful and nice." And

Paramount said, "All right, Warner.

Let's let's give this another go. You

want to come to the negotiating table,

talk with us?" And Warner over the

holidays sat around, thought about it

for a little bit, and said, "Nah, we're

good. We like what we've got with

Netflix." And shareholders got pissed

off. Truly furious. Because from their

perspective, we're talking about $30 a

share for a whole company in cash.

Everyone loves cash. versus 2775 for

part of the company. So, less money for

less of the company. It was more

complicated. It was more muddled. Warner

rejected it again. Paramount said,

"Well, okay, fine. If you don't want to

do that, Warner Brothers board, uh,

we're ready to fire you. We're going to

mount a proxy fight. We're going to try

to take control of your board, uh, cuz

we think shareholders are pretty pissed

off about this and and want a chance to

get their hands on all our cash." So,

they did that earlier this week. Now,

it's come out. Bloomberg first broke

this news. We've confirmed it. Several

other outlets have confirmed it as well.

uh that Netflix is pretty close to

making its bid all cash. So, it's trying

to solve for some of the problems that

shareholders have pointed out. Mostly,

they don't really want to own Netflix

stock, right? They want to own uh they

don't want to own Netflix at all. They

want they want cash in hand. Who doesn't

want cash?

>> Um that's where we are today. And as we

reported earlier right before we, you

know, we're getting on to talk about

this right now, both Paramount and

Netflix have have been making their case

to regulators in Europe, but also in the

US, trying to sort of say, look, we are

the pro competition deal here, even

though remember Paramount, as we know,

doesn't have its own bid yet. It hasn't

been approved. Uh, so that's sort of

where the lay of the land is as we stand

today.

>> So, so much in there. Um, I think one of

the most important pieces is the fact

that Paramount comes back and gives a

better offer. I mean, they said before,

"Oh, we don't trust that you have the

money." Then dad comes along and says,

"No, no, I have the money." And we know

that he does. They make the offer again

and then Warner Brothers says, "No." And

this is interesting because one thing

that we saw from David Ellison before

all of this unfolded, before Netflix was

getting involved, before we even knew

that Netflix had made the offer, is he

wrote this letter to Warner Brothers

saying, "Hey, I think you guys are

biased against me." And something that

you reported is that you've been

speaking with shareholders. Shareholders

think there is a quote inexplicable

personal animus between Zazloff and

David Ellison. This is what you wrote.

So, it sounds like maybe David Zazaf and

the board actually are biased against

David Ellison. I thought it was kind of

a a ridiculous statement, but it sounds

like maybe it's true. What do you think?

>> I I'll be honest. Look, remember when we

first spoke, I thought Netflix had it. I

thought that Paramount had not done

enough to solve the problems, the real

problems that Warner Brothers has. But

time has gone on. They've stepped up the

certainty of their financing. They've

said, "Look, we're willing to negotiate.

please just come to the table with us

and talk to us. And Warner, again, this

is Warner's board. We can't all put it

at D David Zazov's feet, but David Zazov

is also the CEO of this company and has

a lot of influence over this board. Has

just said no time and time again. No, I

might add in kind of an insulting way. I

mean, their last response, as you know,

Ed, was to compare it to a leveraged

buyout, which is not something that sits

well with anybody when you're trying to

talk about how much you care about a

brand, how much you care about these

assets, how you want to steward these

assets. When we think LBOS's, we think,

you know, what private equity used to

do, let's buy an asset up with someone

else's money. Let's strip mine all the

good stuff out of it, and let's make a

ton of cash for ourselves. Screw the

shareholders. Screw the employees.

That's what Warner Brothers compared the

Ellison's offer to. And as we reported,

it was super insulting to these guys. So

yeah, some shareholders really do feel

and certainly my reporting hasn't gotten

to the bottom of this. I would love

David Ellison if you want to pick up the

phone and let me know what you're

thinking here. Um I would love to

understand this, but certainly the

shareholders I spoke with said, "Look,

it makes no sense. These guys have all

the money in the world. And if that

wasn't enough, they've got three

friends, right? These sovereign wealth

funds who have all the money in the

world. Why aren't they picking up the

phone and talking unless Zazlov has some

beef with Ellison? Remember these guys

that went out to dinner together? They

went on walks together. They had all

these conversations leading up to this

auction. Ellison even offered to make

him co-CEO. That's David Zazov, co-CEO

of the combined company. That's not a

joke. That's a real offer. And that was

in a lot of the merger documents. As it

stands, you know, Zazov will make a ton

of money off this either way. So, it's

left to, you know, it's left to our

imaginations what we think. But this is

what M&A bankers call the social issues

of a deal. The price might be right, the

structure might be right, but if two

CEOs don't like each other, if two

boards don't like each other, it's the

same as real life. It becomes hard to

get anything done.

>> Ultimately, this looks like maybe a

shareholder lawsuit. I mean, Zazav has a

fiduciary responsibility

to get the best price, to get the best

offer. If the shareholders are saying we

think the best offer is from Paramount

and he's not doing it because

because I don't know because he doesn't

like him because uh he doesn't like his

dad because they're buddies with uh the

president. I don't know what it is but

doesn't that seem like a lawsuit?

>> Shareholders are always going to sue. In

fact, shareholders already have in San

Francisco I think the very week this

deal was announced. uh shareholders

always want more money and if they don't

get the money they're always happy to

complain. What has happened, right, is

this proxy fight, right? So, this board

fight that that Paramount has threatened

to kick off. And that is the easiest way

for shareholders in the short term to

express how unhappy they are. Now, one

big shareholder, that's a shareholder

called Pentwater, already went on CNBC

and has said, "Look, this is insane.

This is crazy that they're not talking.

We're going to block the Netflix deal.

We're going to vote to block the Netflix

deal because we feel like it's

absolutely crazy to turn down 30 bucks

for this company." Because remember

before we talked when we talked uh the

closest comp to the planned spin-off of

uh from Warner Brothers Discovery was a

company called Versent. That's my former

employer CNBC, MSNBC, a bunch of grabag

assets that were leaving Comcast. That

company hadn't started trading yet. And

everyone kind of thought this company is

going to be a better play than Warner

Brothers Discovery spin-off. That hasn't

been the case. That stock is in the

tubes. It's terrible. And so when that

happened, a lot of shareholders went,

well, Vers has less debt than Warner

Brothers plan spin-off. Uh,

theoretically, it's a better, higher

performing, higherend collection of

assets, and it's trading like crap. No

one wants to touch this thing. If that

thing, that quote unquote quality asset,

it's all relative because it's TV. But

if that quality asset is trading so

badly, what chance do I have of making

up for my $2.75 or sorry, $2.25

off this spin-off? I'd rather go with

something more certain. M

>> um so you know we'll see how this proxy

fight shapes out if they even need to do

it but it's certainly shareholders are

not happy not in the slightest.

>> Something you said earlier we'll leave

it to the imagination why he's not going

with Paramount. Uh you've been studying

this for a while. You've been reporting

on this. You're speaking with sources.

Let's use our imagination. Why do you

think he's saying no? Why do you think

David Zazov doesn't want to take the

deal?

>> That's a tricky one. Um, if I had to

guess, look, Warner Brothers, the

combination of Warner Brothers and

Discovery, it was supposed to be a

crowning achievement for Zazov and John

Malone who helped orchestrate this deal.

And that was almost that was 5 years

ago. Now it's 2021. Um, you were going

to marry these two assets and you were

going to build something better and

bigger than the sum of their parts. And

to do that, they took on a lot of debt,

a lot of debt. And to his credit, David

Zazov has managed to pay down a

tremendous amount of that debt. the

company is far healthier uh financially

than it was when it merged, but that

wasn't reflected in the stock price,

right? The stock ticked down and down

and down really until this bidding war

started, which by the way created tens

of billions of dollars of value for

shareholders. So, kudos to Azoff for

that in all seriousness. And then you

have this guy, you've got Larry Ellison,

uh, and you've got his kid David who

have all the money in the world and they

go and they pick up one of the most

storied studios in the planet. They pick

up Paramount just like that cuz they

want it cuz it's nothing to them. And

now you're David Zazov. You're sitting

there. There's been a lot of reporting

about his his sort of his the way he

approaches the job as CEO. And there's a

great story in New York magazine about

this. I think it was New York magazine

about how he actually has and uses the

desk of Jack Warner, the father, the

creator of Warner Brothers. So there's

some implication that he actually thinks

of himself as a modern-day mu uh movie

mogul.

>> And yet he hasn't really been successful

in those ambitions, right? he hasn't

managed to give the company the

financial relevance that he sought.

David Ellison, on the other hand, has an

unlimited checkbook. And so, you kind of

have this interloper. This guy, to be

fair, he's been a producer for a long

time, but this guy who's never run a

major studio, who's certainly never run

a media conglomerate, who suddenly is

buying up everything for sale. In other

words, is doing exactly what David Zazov

wanted to do, but was never able to get

done. That's just a guess. I haven't

talked to Zazov. I haven't talked to

Ellison about their psychologies or how

they feel. I would love to. that's never

going to happen. So, that's my best

guess. But it also makes sense. It's

human nature, right? You try to do

something, you don't succeed at it, and

then you watch someone just waltz in and

do it instead of you, you're you might

feel a little resentful. Again, totally

guess. No sourcing here. Um, but if I

had to put money on something, I I

wouldn't I'd put a couple bucks on that

for sure.

>> Fascinating. I think we could talk about

this for hours, but we're going to have

to let you go here. Rohan Gwami,

business reporter at Sema 4. Rohan,

really appreciate it. Thank you,

>> Ed. Always a pleasure. Thanks so much.

>> We'll be right back. And if you're

enjoying the show so far, be sure to

like and subscribe to the ProfG GP Pod

YouTube channel at the link below.

Support for the show comes from

LinkedIn. It's a shame when the best B2B

marketing gets wasted on the wrong

audience. Like, imagine running an ad

for cataract surgery on Saturday morning

cartoons or running a promo for this

show on a video about Roblox or

something. No offense to our Gen Alpha

listeners, but that would be a waste of

anyone's ad budget. So, when you want to

reach the right professionals, you can

use LinkedIn ads. LinkedIn has grown to

a network of over 1 billion

professionals and 130 million decision

makers according to their data. That's

where it stands apart from other ad

buys. You can target your buyers by job

title, industry, company role,

seniority, skills, company revenue. All

so you can stop wasting budget on the

wrong audience. That's why LinkedIn Ads

boasts one of the highest B2B return on

ad spend of all online ad networks.

Seriously, all of them. Spend $250 on

your first campaign on LinkedIn ads and

get a free $250 credit for the next one.

Just go to linkedin.com/scott.

That's linkedin.com/scott.

Terms and conditions apply.

>> We're back with Profy Markets. Well, the

past few days have been extremely busy.

We had the situation in Iran. We had the

fight between Trump and the DOJ and

Jerome Pal. We had this controversial

inflation report. And all of this has

made it a little bit difficult for us to

focus on what we usually focus on, and

that is earnings. And as a result, there

was a pretty interesting report that we

didn't cover yesterday, and that was

Delta's earnings report. So before we

end today's episode, we're just going to

quickly cover it now. So Delta had a

pretty decent quarter. They reported

record revenue. They also beat

expectations on earnings. But that is

quite surprising because when you dig

into the numbers, what you'll find is

that their main cabin sales actually

fell by 7%. Which raises the obvious

question, how is it that they had a

pretty good quarter despite the fact

that main cabin sales were down? And the

answer lies in the growth of premium

cabin sales, i.e. first class tickets.

That business grew by 9% year-over-year.

And in fact, for the first time in

Delta's history, the premium cabin

business is now larger than the main

cabin business. Premium tickets

generated 5.7 billion in revenue.

Regular tickets generated 5.6 billion in

revenue. Put another way, Delta's growth

is now being kept alive by rich people.

Now, if you're a regular listener, you

know this is a theme we talk about a

lot. This divide in America between the

rich and the poor, the K-shaped economy

as people are talking about it and the

extent to which that divide is actually

driving the real economy. The most

important data point that we flagged

last year was this data from Mark

Xandandy which found that the top 10% of

earners in America are now responsible

for half of all the consumer spending.

That number has never been higher. And

this shocked us, not because it was

necessarily surprising to us, but

because it was just such a vivid

illustration of something that we

already kind of suspected, but weren't

fully seeing. Well, now we're seeing it

at the company level. Now, we're seeing

it reflected in the earnings of some of

the most iconic companies in America, in

this case, Delta. And in fact, CEOs are

now outwardly acknowledging this. Delta

CEO Ed Bastion said, quote, "There's a

lot of discussion about the K-shaped

consumer. Our consumer happens to sit

right at the top end of that K." And

it's striking the extent to which the

K-shaped is now openly being recognized.

It's no longer some theory that people

talk about on podcasts. It is an actual

reality. It is a law of business that

companies are expected both to

understand and also to capitalize on.

And that is exactly what Delta has done

here in this earnings report. And it's

also why they are talking about it

because they know investors feel better

if they see that your business is

specifically catering products to the

nation's very richest people. Those are

the consumers that matter. So those are

the consumers that you need to own and

that is what Wall Street wants to see.

Now, to be honest, I'm not sure if this

is better or worse than what we had

before. When people would theorize about

this inequality problem, they talk about

the K-shaped economy, they discuss it

intellectually versus what we have now

where people and CEOs seem to simply

throw their hands up and accept it as

some principle of the universe. Yeah,

the K-shaped economy. Oh, yeah. That's

just the way it is. I actually don't

know what is worse. Either way, what is

clear now is we have gone from theory to

reality. We've gone from bargaining to

acceptance. The gap is getting bigger.

The rift is getting wider and we are now

watching this play out in earnings.

Thank you for listening to Profy Markets

from ProfG Media. If you liked what you

heard, subscribe to our YouTube channel

and also tune in tomorrow for our

conversation with Scott Nations.

Interactive Summary

Ask follow-up questions or revisit key timestamps.

The video discusses recent market trends, focusing on bank earnings, political influences on the market, and the potential acquisition of Warner Brothers Discovery. Major indices ended in the red for a second day, with Nvidia and bank stocks declining. Oil prices dropped, while gold, silver, and copper hit record highs. Bank earnings presented a mixed picture, with major banks like Citigroup, Bank of America, Wells Fargo, and JPMorgan Chase seeing stock price drops despite some beating revenue and profit estimates. This downturn was attributed to mixed results, profit slides, and political pressure, including a proposed cap on credit card interest rates and the DOJ's investigation into Jerome Powell. The discussion delves into the divergence between positive bank results and negative stock reactions, suggesting high market expectations. It also touches upon the potential sale of Warner Brothers Discovery, with Netflix reportedly preparing an all-cash bid, and Paramount launching a proxy fight. The segment on Delta's earnings highlights the growing influence of premium cabin sales, driven by affluent consumers, and the broader economic trend of a K-shaped recovery where the wealthy disproportionately drive consumer spending.

Suggested questions

6 ready-made promptsRecently Distilled

Videos recently processed by our community